Broadcom (AVGO) vs Qualcomm (QCOM)

Broadcom (AVGO) and Qualcomm (QCOM) are both U.S. semiconductor heavyweights, but they offer very different mixes of growth, risk, and income within the same sector.

Business models and end markets

Broadcom is now primarily an infrastructure and data‑center story, with a large and growing exposure to custom AI chips and networking for hyperscalers, plus a sizeable enterprise software segment from the VMware acquisition.

Qualcomm is still dominated by mobile handsets and related licensing, while steadily building automotive and IoT revenue streams and pushing on‑device AI in smartphones and PCs.

Practically, AVGO is a levered play on continued AI capex and cloud/data‑center build‑outs, while QCOM is more tied to the smartphone cycle and diversification into auto/IoT connectivity.

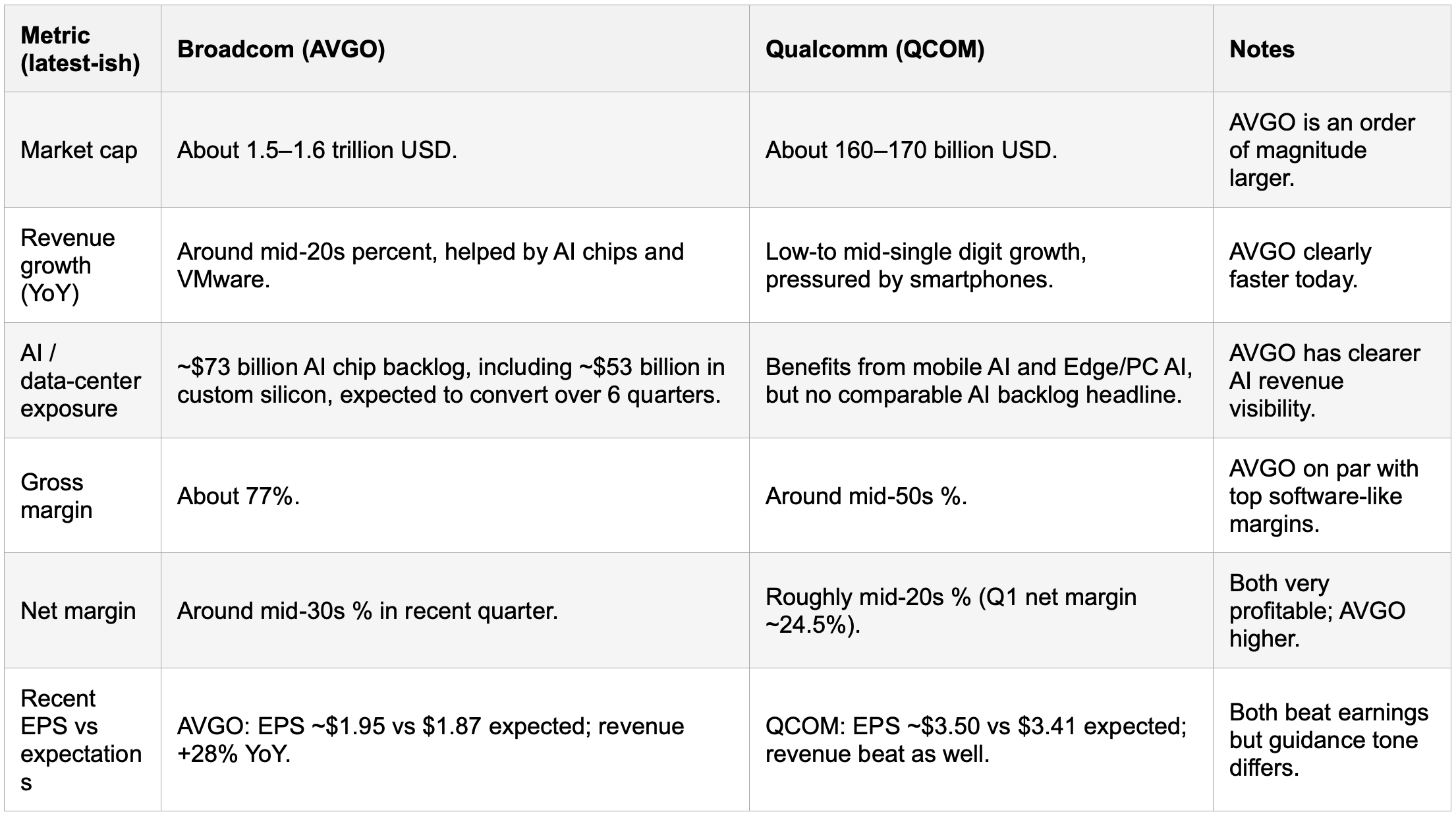

Size, growth, and profitability

Takeaway: AVGO currently looks like the higher‑growth, higher‑margin compounder, while QCOM is profitable but growing more slowly as it works through smartphone and client concentration issues.

Valuation and income

Broadcom trades at a rich valuation on trailing metrics: P/E around the high‑60s to low‑70s in some snapshots, with a price‑to‑sales ratio above 25, significantly above the semiconductor industry’s top quartile.

Qualcomm’s valuation is materially lower, with a P/E roughly in the low‑30s and forward multiples around the high‑teens to ~20x EPS in some analyses.

On cash returns, AVGO offers a modest dividend yield of around 0.7–0.8%, reflecting its big price run‑up.

QCOM historically offers a meaningfully higher yield (roughly in the 2% range), making it more appealing to income‑oriented investors willing to accept slower growth.

In simple terms, AVGO is priced like a premium growth franchise with embedded AI optionality, whereas QCOM is closer to “core value/GARP” in the same sector.

Balance of risks

Broadcom (AVGO)

AI capex cyclicality: A huge portion of the thesis rests on hyperscalers maintaining or increasing AI infrastructure spending; a pause or digestion period could hit growth and multiples together.

Concentration risk: Significant revenue tied to a handful of cloud giants and to large custom‑silicon contracts.

Valuation risk: With a price‑to‑sales and P/E well above most peers, any earnings disappointment or guidance cut can result in sharp drawdowns.

Integration/execution: Managing a large software portfolio (VMware and other acquisitions) alongside the chip business adds operational complexity.

Qualcomm (QCOM)

Smartphone dependence: Despite diversification, roughly half or more of revenue still comes from handset chips, and management has guided to weaker near‑term smartphone demand due to memory shortages and macro factors.

Customer in‑sourcing: Apple and Samsung are designing more of their own chips, while MediaTek competes aggressively in Android; this can pressure Qualcomm’s share and pricing power.

Near‑term guidance: Qualcomm recently guided next‑quarter revenue and EPS below Street expectations, which weighed on sentiment and the share price.

Regulatory/IP risk: Ongoing exposure to antitrust and licensing disputes in various jurisdictions because of its IP‑heavy model.

In essence, AVGO’s main risk is paying too much for a still‑strong AI story, while QCOM’s main risk is that its diversification may not fully offset long‑term erosion in core handset economics.

Which type of investor each fits

Broadcom may fit investors who:

Want maximized exposure to AI/data‑center infrastructure rather than consumer devices.

Accept higher valuation and volatility in exchange for faster growth and very high margins.

Are less focused on current yield and more on long‑term compounding and potential buybacks/dividend growth.

Qualcomm may fit investors who:

Prefer a more diversified revenue mix across mobile, auto, and IoT rather than a pure AI bet.

Want a higher starting dividend yield and more moderate valuation multiples.

Are comfortable with cyclical handset exposure and willing to wait for auto/IoT/PC AI to become larger profit drivers.

A simple illustration: if you believe AI data‑center spending will remain elevated for many years and you can live with premium pricing, AVGO is the more aggressive choice; if you think smartphones and edge devices will quietly compound with less multiple risk, QCOM may be the steadier, income‑friendlier option.

Disclaimer: This discussion is for informational and educational purposes only and does not constitute financial, investment, or trading advice. It does not consider your individual objectives, financial situation, or needs. Always do your own research and consider consulting a licensed financial professional before making any investment decisions.